Off-Peak--The U.S. Incentive Auction

Why the spectrum auction of the century missed the market’s incentives.

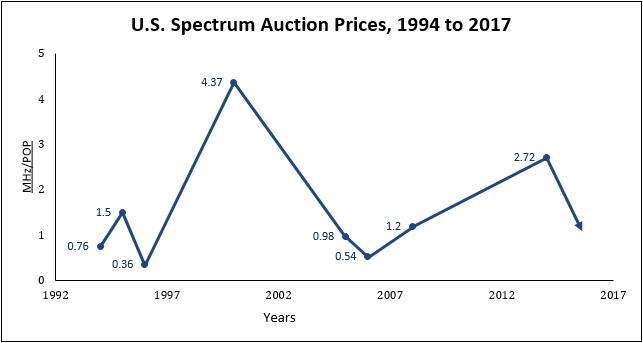

Auction prices follow long cycles, as the figure below shows, and they can be subject to surprises, as we have learned from cases on which we advised bidders. Sometimes a government agency—not the one running the auction—intervenes to affect the prices, other times a bidder is trying to scare the competition away from the next auction, and then there are the security breaches, the signaling between bidders, and the auctions where fewer bidders show up than there are spectrum blocks for sale.

We don’t know if any of these things happened at the Incentive Auction. We do know the expectation it would exceed all past spectrum auctions in total proceeds was not met—or even came close. We warned this would happen two years ago at a spectrum conference but few paid attention. Euphoric predictions flowed. What the auction has exceeded is both the complexity and the time period of any previous spectrum auction, starting as it did March 29, 2016 and ending just days ago.

The auction generated $19.6 billion in bids—possibly to be amended incrementally upward in the post-Forward Auction Assignment Round still to come. This compares with $45 billion for the AWS-3 auction in 2014/2015 and $34 billion for the UK 3G auction in 2000, which represented 2.5% of UK GDP. By comparison the Incentive Auction has generated less than 0.1% of U.S. GDP, and hasn’t all been collected yet. Plus it has cost the FCC a quarter-billion dollars to run. Finally, on a per MHz/POP basis, the price paid in the Incentive Auction, still being calculated, is likely to approach the low points experienced in 1994 and 2006 (see the figure).

Kalba International, 2017So surprises? Yes, big ones. How to explain them?

Kalba International, 2017So surprises? Yes, big ones. How to explain them?

First of all, there is the long view, as reflected in the figure. Spectrum auction winning prices actually drop as much as they rise, notwithstanding the common view that spectrum value can only go up. They make real estate crashes, typically involving 30% to 50% drops, look stable. In large part this is due to the financial cycle. So quite possibly the financial community was less sanguine about the value of the spectrum than the mobile operators.

Second, competition from “dark horse” bidders did not emerge the way it had during the AWS-3 auction, when DISH, the satellite TV provider, became a big factor. Three operators primarily drove demand—namely, AT&T, Verizon and T-Mobile, with the push from large cable TV bidders not evident. (One of the obvious horses, Sprint, did not even participate in the auction, deciding that its small coverage deficit could be handled through price discounting rather than by acquiring low- band frequencies.)

This brings up an underlying point. As capacity-guzzling apps grow the need for spectrum in urban areas is growing, with wide-area coverage becoming less critical. This started to be apparent in the 700 MHz auction eight years ago, with some bidders preferring concentrated zones over large regions. With the 600 MHz frequencies not being available for some years (after repacking and clearing of the broadcast users), their benefits became less clear.

What does this say about future auctions? Assuming an open spectrum trading market is not allowed to emerge (possibly the best option, given how protracted, costly and erratic auctions can be), the dates and methods selected to conduct auctions will continue to have a large influence on bidding prices. What is clear is that an auction process, first proposed in 2010, whose operational results will not be evident until a decade later may not be the way to go.

Send us your Comments or learn about our Spectrum & Licensing Practice

View Printer Friendly Version

View Printer Friendly Version